NOTE: I started writing this entry a couple of weeks ago, before my posting on Tax Reform and the Middle Class - which addresses the New York Times' claim in a recent article that home mortgage interest deductions created wealth disparity. Perhaps it is not the home mortgage interest deduction - which has been around since after the war, but the 401(k) which is a more recent invention. Perhaps.

Did the 401(k) create wealth inequality?

Income inequality and or wealth inequality (which are two separate things) have been in the news a lot lately. People on the Left have harped upon an increase in the disparity between the wages and wealth of the very rich and the very poor as a sign of a breakdown of our society.

Many on the Left posit that the cause of this disparity was the Bush tax cuts of the 2000s, which reduce the tax rates on the very rich. However this answer is too facile and easy and doesn't stand up to scrutiny.

While marginal rates were slightly reduced during the Bush era, the slight decrease of a few percentage points really isn't enough to account for huge increases in wealth by the very rich. What's more, marginal rates are rarely paid by the very wealthy as Mitt Romney aptly illustrated. The very rich can afford to incorporate and pay themselves and capital gains and pay only 15% capital gains tax. And that is a pretty old law which hasn't changed in recent years. Thus, the tax explanation isn't quite the right answer.

What has changed in the last two or three decades is we've become more of an investor nation, and not by choice. With the demise of the defined benefit pension and the rise of the IRA and 401(k), ordinary citizens are forced to invest for their future rather than rely on fixed benefit defined-benefit pensions.

The result of this is a lot of small investors such as myself are getting into the stock market and buying stocks without really knowing what we're doing. As I've mentioned before, the outrageous stock prices for many of these tech companies are not based on what the people who founded the company paid for the stocks, but what the last investor in paid. In other words the last chump who buys a share of LinkedIn or Facebook is the one driving the price through the roof, and technically this is a small investor paying the top dollar.

And as investors, we want to see the maximum return and our 401(k) because we all want to be rich and have a healthy retirement. So we demand high rates of return on a quarter-by-quarter basis, sometimes on even a monthly or daily basis without regard to long-term profitability or stability of the company in question.

To achieve these spikes in share price, we have incentivized company managers and fund managers with arrangements which pay them in stock options or based on share price increases. This motivates these managers to jack up the stock price is high as possible in order to maximize their own personal profit. As a result this can result in a payday in the millions or even tens of millions for some lucky managers, and smart managers figure out ways to make the stock price of their company soar.

And one way to achieve these results is to cut the pensions and benefits of the poorest workers for that company. The poor can't afford to invest in a 401(k) and they are now even less likely to receive even a modest pension from a company after 30 years of hard work. The middle-class profits from their 401(k) investments, and the investor and manager class profits hugely from stock options and other deals that yield staggering incomes.

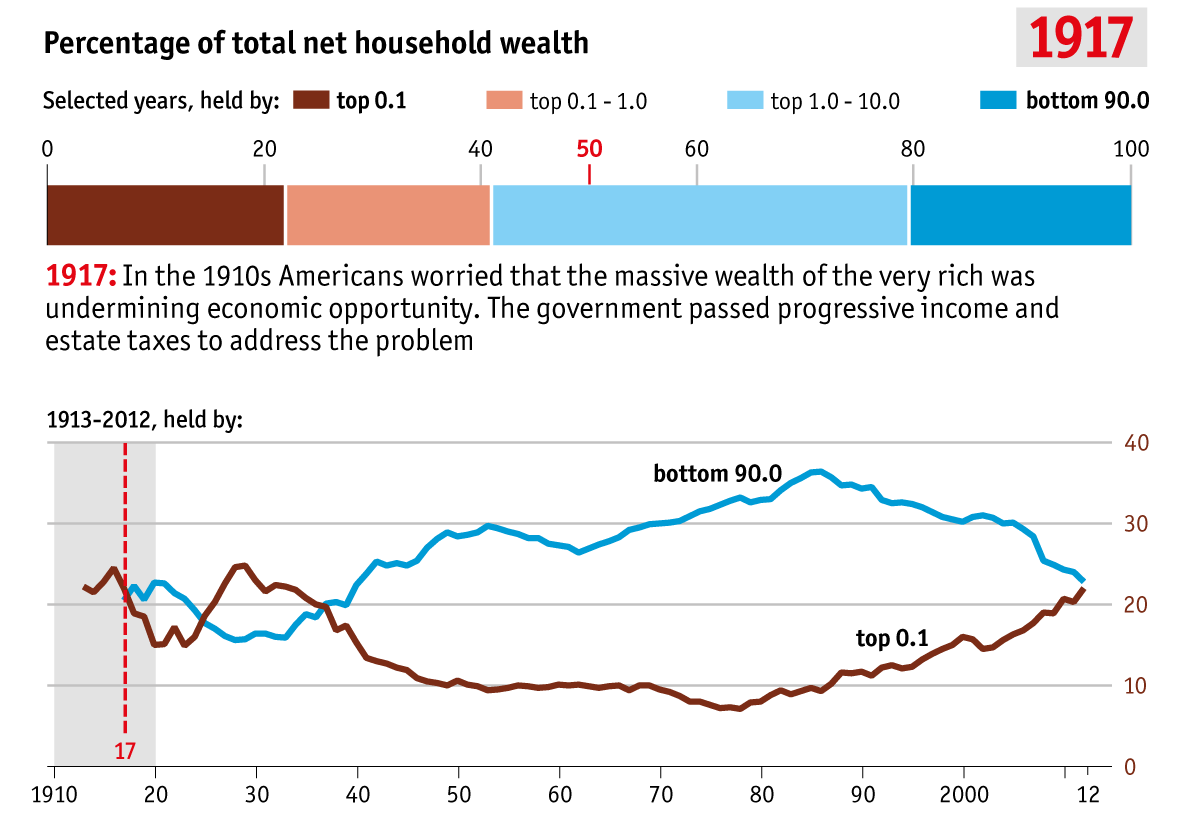

Draw the chart - does wealth inequality start after World War II when the home mortgage interest deduction was created? Or does it begin shortly after 1978 when the 401(k) was created - and accelerate throughout the 1980's and 1990's as more and more companies dump pension plans (even the Federal Government!) and adopt 401(k) type plans. It is an interesting thought.

Of course, it was not always this way, even for small investors. My mother used to buy stocks when I was a kid, and the cost of buying a stock was rather steep, as you had to go through a stockbroker who charged a pretty hefty fee. I remember selling some stock my grandfather left me back in the 1980s and paying $30 to $50 just for the privilege of selling the stock, and I believe he was doing me a favor at the time by charging me so little (It was Republic Bank of Texas stock, and a good thing I sold it as it went belly-up).

Today, we have low-cost trades and even zero-cost trades which allow small investors to buy even one share of stock with no little or no transaction costs. In the old days, my Mother would hold physical stock certificates in her safe deposit box and have the dividends reinvested or mailed to her and a check once a quarter. You bought and held stocks for the long-term, rather than buying and selling based on where you thought the market was heading.

And, as you might imagine, share prices were more stable back in that era. It is only in recent years since the introduction of the IRA and 401(k) that we were seeing wild swings and share prices. I believe this can be directly traced to the increased number of little people playing the market and moreover people feeling they need to make it big in a hurry in order to fund their retirement.

My mother's time was also the before the Internet. So the idea of swapping stock tips online or going to websites which discuss strategies for buying and selling stocks was just alien. Today, there any number of sites you can visit where people cheer-lead the idea that you should churn your investment account in order to "cash in" on great bargains and deals, most of which are spurious. The idea you can beat the market has always been a dream, but in general it's been a false dream.

The other half of the wealth disparity and income disparity equation is the decline of wages for the middle class. The reasons behind this are also less interesting than those proposed by the Left. The big problem is that high paying union jobs have largely going away in America. Companies hire fewer people as efficiency has improved thanks in part to improve machinery and robotics. It takes half the number of people to build a car today and that in the past. Part of this also is that car makers farm out the production of parts to independent companies many of which are non-union and/or located overseas. When I worked at General Motors, we made every single part of the car except for the tires the paint and the gasoline we put in the tanks. Today, General Motors merely assembles parts into cars, and most of these parts are made and independent factories or even overseas.

And again, the reason why companies pursue this cost-savings is the expectations of investors - the middle-class who wants high rates of returns on their 401(k) and damn the consequences! So companies have to cut costs to the bone to appease Wall Street, and by extension, the middle-class 401(k) investor. We have met the enemy and he is us.

One could argue also that is the supply of labor has increased, and the demand for labor decreased, the value of labor has decreased as well. Whether we can go back to the union era of high wages - often four to five times the prevailing rate - is questionable. It would be propping up an economic system that would not be sustainable and eventually collapse - as our economy did in the late 1970's.

But I think another aspect of this trend, at least with regard to wealth disparity is that many in the middle class today have dissipated their wealth by purchasing toys and services rather than saving and investing. Defined benefit pensions were a means of forced saving for the middle and lower classes - which kept them from sinking into poverty in old age. While the new investor class may have driven stock prices crazy, it represents only a portion of the middle class and very little of the lower classes. The alarming fact is that very few people have saved much for retirement or saved anything at all. Many people complaining of living "paycheck-to-paycheck" have several vehicles parked in their yard as well as a deluxe cell phone plan and every channel of satellite or cable television.

When I grew up - I came from a upper-middle-class home - we didn't have cable television largely because it didn't exist. And cell phone plans were also nonexistent - we had one phone in the house and we were always nagged not to stay on too long because the phone bill would be too high. Most families only had two cars, compared to the five or six you see populating the driveways of many suburban households today. If young people wanted to drive they borrowed dad's car. And when you went off to college, your parents give you a ride there - you didn't have a car on campus.

Our apparent wealth has increased since then, as our generation has decided to spend more and save less. And with the plethora of inexpensive consumer goods available to us it is easy to spend a lot more.

While this does not account for income disparity, it does show how wealth disparity can be altered not by external forces but by internal ones - our choices on how to spend our money. The irony is to me, that even back in the day of fully funded defined benefit pension plans, my parents still saved money and invested in stocks, rather than rely only on the promises of a pension plan. They also make regular payments on their mortgage and paid it down rather than continually adding to their debt load through refinancing, which was almost unheard of back in the sixties and early seventies.

Thus, when retirement came, my parents had a house that was nearly paid for, some money in the bank from investments, and a small pension and Social Security. My parents never had the fancy cars, jet skis go fast boats. My parents never had a deluxe diesel pusher motorhome, even though my father was a vice-president of his company.

Today, I see a lot of people of fairly modest means with all of these sorts of toys, usually financed on time. And as I illustrated in a number of earlier postings, it is very easy to upside down on these things end up paying for the rest of your life for what was a transitory pleasure.

This is not to say that the Bush-era tax cuts had no effect on wealth or income disparity, only that the effect was fairly trivial. Cutting or increasing marginal rates really only affects the upper middle classes, such as doctors and dentists and other professionals who make in the mere hundreds of thousands of dollars. They don't have quite enough money to figure out ways to avoid paying income taxes and pay themselves and capital gains instead. Although lately, more and more are figuring out how to do this which is why your Dentist is now an LLC and not a solo practitioner.

In other words if you view the tax code as a wealth transfer scheme, which it is to some extent, particularly with graduated marginal rates, it has not been a very effective means of transferring wealth from one group to another. On the other hand, the proposals by the Trump Administration will basically cut what little wealth transfer feature our present tax laws have.

Sadly, I believe that even those Draconian tax changes will not be the cause of the next wave of wealth transfer, at least not directly. By cutting taxes to the very wealthy by such huge margins, without having corresponding spending cuts, we will increase our deficit spending even further. Over time, this could lead to rapidly accelerating inflation which would have two interesting and opposite effects.

For the middle class which is saved nothing and borrowed everything, hyperinflation will be a blessing, as they will pay it back old debts with new dollars which are worth far less. Of course, when they try to borrow more money they will find the interest rates in the double digits.

The second effect will be even more devastating, is it will basically wipe out the savings of those who did choose to save, as their retirement plans become worth less and less as the new dollars purchase less over time.

But it is an interesting thought, though. Did the 401(k) create wealth disparity? By making the middle-class and upper-middle-class into investors, we've pushed the market for greater and greater returns, lining our own pockets and really rewarding those who run such companies or run investment houses. Meanwhile the lower classes have their wages and benefits and most important, their defined benefit pensions cut. And the middle-class people who didn't bother to save under this new plan find themselves part of the new poor.

UPDATE: I am not sure whether this is true or not, it is just a thought that struck me. And it makes more sense than the New York Times' argument that home ownership caused wealth disparity!

{kind=link}